lol. Thats why its funny…

How do you afford things that’s very little

Charge more

3 Likes

Just spitballing here, I don’t know Chad’s actual numbers (and I think it’d be rude to ask). But…

12 workdays per month, x 6 hours per day, x $125/hr = $9000/month

x 11 months (guessing here; Chad is in Louisiana) = $99k/year

Or approximately $65-$75k take-home, after taxes and expenses. That’s a pretty darn comfortable living in many parts of the country, especially if you’re frugal. And it’s still low enough that a married couple can get health insurance subsidized through the ACA

2 Likes

I live well within my means. I am also not married, no kids, no house note and no vehicle note. That helps a lot.

Not asking for his numbers and I was afraid that would come off bad I am just saying That’s not a lot of hours to pay bills and have a retirement of course everyone’s economy and spending habits are different and who knows maybe he has a side hustle or is a master in the stock market.

Feel free to PM me

1 Like

Who lol

You  . I saw you had some questions about how 99k gross could work out to $65k take-home, but you deleted your comment. So I figured you might want to keep that conversation private.

. I saw you had some questions about how 99k gross could work out to $65k take-home, but you deleted your comment. So I figured you might want to keep that conversation private.

But the invitation is open to anyone. Happy to share some numbers privately.

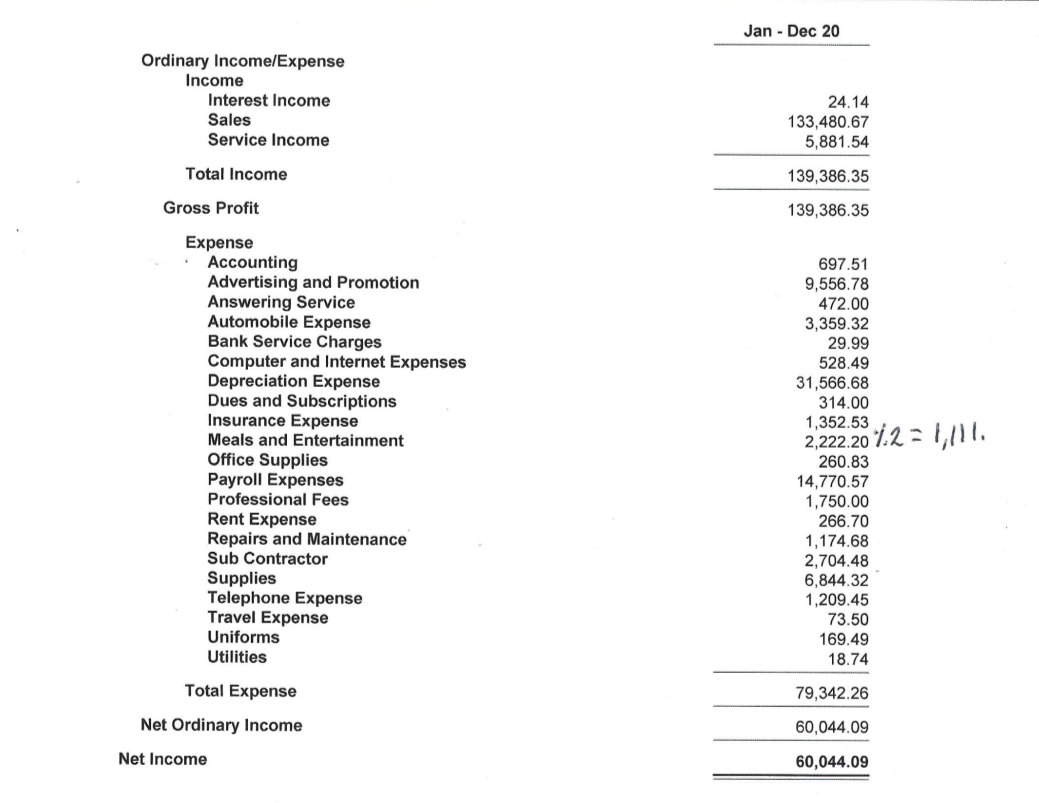

Nope not private. I went from 139k to 60 k net so very confused. Granted I had $30,000 that I depreciated on the year 2020 instead of depreciating it over 5 years. I also had a part-time employee that cost me 14 grand so together there’s 45 grand but look how much I lost after expenses. So how could someone go from 99 to 65 to 75 after expenses plus the government. Seems like just after the government you’d be from 99 to 60

Well guess I can’t overlook the 45 k. If I didn’t have a 30k truck or payroll that adds 45 k to my income but then more tax so not sure how that would have squashed out. I’d like to net $100 k after expenses take home in my pocket.

Talk to your cpa and ask him what if’s , everyone one is different. A single young male will always pay more in taxes than a older married male with kids and a mortgage .

Also I hope you’re an LLc or s Corp , that will help with taxes . You might have to put your self on payroll(w2) with quarterly distributions , to save taxes . Anyways talk to your cpa

1 Like

I’m a Sole Proprietorship but have been told to become an LLC for liability reasons.

Nobody pays more taxes than sole proprietorships. Ask your cpa about making the s-corp election. You can search my name and s-corp for more info.

Also, a solo operator in ‘sustain mode’ (vs. what you’re probably experiencing, ‘growth mode’) can really trim business expenses to a minimum. Especially if you’re focusing on just one or two services.

I’m betting Chad’s marketing budget is similar to mine: almost nonexistent.

Then you consider: get a low cost to operate work vehicle, home office (no shop rent) etc. and there’s not a whole lot other than your insurances and basic supplies to keep you in business.

If you want some numbers, here you go:

2019

We had 102k gross sales.

After business expenses (including employer portion of payroll taxes) we had a “household gross income” of $77kish. That was split between about $41k in payroll and the rest in quarterly distributions.

We paid in $8kish in employee portion payroll taxes, and about $5k in estimated taxes on the distributions (but much of that actually was applied towards APTC repayments for making more than we expected; it was really for health insurance, not taxes).

That brought our household income down to $64k take-home, after taxes.

And we had a fairly decent sized refund to apply towards 2020 taxes. So in actuality, our “take home” would’ve been more than $64k, had we paid in less on the estimated taxes.

Also, we were informed after the fact by our cpa, that for our situation we could have taken a smaller salary, perhaps around $35kish, and taken a little more in distributions, saving us even more.

So that’s where I come up with $99k possibly working out to $65-$75k take home. Controlling expenses, and effective tax planning.

I am a one person window washer. I do strictly just windows and charge competitive prices but am very efficient. My vehicle set up is great because I have all my tools at all times, it’s clean & accessible and I have a low cost but efficient pure water set up and I’m fast at windows/skilled. No office just my phone & laptop and print very little as almost all of my customer interaction is email or text. Also getting to a point where I’m able to advertise less. However less cost is more money in your pocket but less write offs higher taxes so not sure how that works.

I have a 2014 Nissan NV200 that runs and looks like it’s brand new but was only 14 k. Could have got a smaller one for less gas but would have traded off effiency.

2 Likes

To start with, “the more you make, the more they take.” But as pointed out in the book “Simple Numbers”, a big tax bill isn’t the worst thing; it’s evidence that you’re profitable. And the tax man is only going to be taking a slice of that pie.

There’s a lot you can do to optimize your tax situation, though. You are at a point where you would absolutely benefit from restructuring as an S-corp. instead of all your profits being taxed as self-employment income, you would pay yourself a small but reasonable salary as a W2 employee, and then take quarterly profit distributions to supplement. That additional income is only taxed as “normal income”, at the standard tax bracket. There’s no SS/FICA collected on those profits.

I can’t make any promises, but I’m betting you’d save $5-6k/year at least by restructuring. Say for example you had $40k in distributions: 40,000 x 15.3% = $6,120 saved in SS/FICA.

Also, I just looked at your P&L sheet again. So your $60k is after taking $30k in depreciation on something (I forget what you said that was for)

But that’s different from what you’re able to pay yourself. That $30k didn’t actually come out of your account all at once, right? It was financed I assume, but depreciated all at once for the write off (which for your situation, was probably a smart move).

Also, $9500+ in advertising. That won’t always be that high, if you plan on remaining a solo op. I think our advertising this year was around $1k, and included yard signs, our website hosting, and lettered shirts.

Thanks for sharing your full P&L sheet, btw. Quite a few people are comfortable throwing out their gross numbers for the year, but there’s rarely any reference to their expenses and what they actually got to keep out it.

2 Likes

A lot of useful info here.

I’m real curious what my numbers will be my 2nd year. My first year I was at a loss so paid no tax.

I’m just curious, so it looks like I have an LLC. Doesn’t specific what, etc so I believe just an LLC.

From here I can go the S-corp route or the C-corp route I believe?

I could probably look up what c-corp is and learn about it but when should I consider going to the S-corp route?

From my limited research, I think C-corp becomes useful when you have a number of employees. Otherwise it can cost you more in taxes and paperwork, IIRC. (Also, I don’t believe you can go C-corp as an LLC. It’s an actual corporate structure.)

S-corp is really more a tax classification than an actual “structure”. You can make the s-corp election as either an LLC (Limited Liability Company) or a traditional Inc.

It’s what’s known as a “pass through entity”; profits are not taxed at the corporate level. They are passed through to the shareholder(s) and taxed at the individual level, at the standard tax bracket (sans SS & FICA).

Hope that doesn’t make things more confusing.

Without making the s-corp election, a regular LLC is also considered a pass-through entity, but the profits are taxed to the shareholder(s) as self-employment income, and you pay SS & FICA on the full amount. That’s what I’m guessing you’re set up as, @Narcos.

If doesn’t all make 100% sense, that’s ok. It took me until year 2 or so of actually being incorporated, before it started to really click in my head. I like math, but I hate tax codes and the vernacular that comes with them. You’ll have to learn weird concepts like “basis” and “shareholder contribution”. Even words like debit and credit have a weird reversal in meaning. It’s nuts.

2 Likes

Exactly, you have to find a happy medium place that works for you . You might kill yourself to make that net 100k or you can take it easy and net 70-60k. Again talk to your cpa . Also if you haven’t yet, pick up some business books on finances and taxes

3 Likes

I’m clearly in the minority here, so I’ll share. I have 12-15 cleaners depending on time of year and how many part-timers on staff. Full time field manager, full time office/operations manager, part time office assistant. I work 4 days a week, 5-6 hours a day. In 2019 (last year before global pandemic) I took 11 weeks of vacation.

It’s all about personal preference. I built my business this way intentionally because it’s what I want. Everything in life is a trade-off. I trade headaches of employees for lots of time off and more income, but that’s my personal choice. For me, it’s worth it, but I wouldn’t tell anyone there is a better or worse way to do it.

There is definitely a tipping point where if you’re going to add employees, you kind of lose money until you grow big enough to have a handful of employees, as Narcos said. We are structured as an LLC that has elected to file as an S-Corp. For my situation that was best for taxes.

Do what makes you happy. If you want a big company, grow a big company. If you want to work alone or with a helper, then do that.

8 Likes